FX – Friday Global Currency Review & Forecast For 4-15-16

The Dollar Struggles To Regain its Footing

The dollar was weak all week until mid-week. On Tuesday, Dallas Fed President Rob Kaplan warned the Fed would not wait too long to raise rates and that a rate hike may be coming soon. His comments had little impact on the dollar as the Dollar Index* sunk below 94.00. Enthusiasm for the dollar was tempered by comments from Philadelphia Fed President Harker urging that the Fed delay another rate hike until they see more inflation. Neither Messrs. Kaplan nor Harker are voting members of the Fed’s policy making committee. As such their comments didn’t have much of an impact on the dollar.

Later on Tuesday, another non-voting member Richmond Fed President Lacker, said that four rate hikes were appropriate in 2016. Mr. Lacker’s comments gave a boost to the dollar. Mr. Lacker’s comments, however, run counter to revised Fed guidance of two rate hikes in 2016.

The dollar continued its rebound on Wednesday even as lower than expected retail sales especially in autos, clothing and restaurants were reported. On Wednesday, U.S. producer prices were reported to have fallen 0.1% vs an expectation that they would have risen. Fed Chair Janet Yellen and Fed officials have often stated that they would like to see significant evidence of inflation increasing towards their target of 2% before raising interest rates.

While weak, non inflationary U.S. economic data might signal that the Fed would hold off on further rate hikes (despite the statements of on voting Fed members to the contrary) and might have normally weakened the dollar further, overseas news prevented the dollar from falling further and helped it rebound. The Dollar Index rose to over 94.70 in mid-week trading.

The Dollar vs. the Japanese Yen

In recent weeks the Japanese Yen has strengthened significantly vs. the dollar, causing the Japanese officials to publically muse whether they should intervene to weaken the Yen against its “one-sided” rally vs. the dollar. Japanese chatter re intervention to weaken the Yen helped boost the dollar mid week. The International Monetary Fund’s mission chief for Japan weighed in on the matter saying he saw no cause for Japan to intervene and that Japan should focus on domestic policies rather than currency interventions.

The Dollar vs. Euro

The dollar also regained ground after the mid week report that Euro zone industrial production was down the most in 18 months. Perhaps the U.S. economy is weakening, but Europe may be weakening more.

The Dollar vs. the Chinese Yuan

The Yuan strengthened against the dollar as recent economy news from China signaled that the Chinese economy may have reversed its slow down over the past two months and reports of a hard landing were perhaps unfounded.

The Dollar vs. the British Pound

Brexit fears continue to pressure the pound with the IMF warning that a U.K. vote to leave Europe would damage the UK and global economies. Economists speculate that a Brexit would cause the Bank of England to cut interest rates which might weaken the pound further.

The Dollar vs. the Canadian Dollar

The Canadian dollar has risen sharply with the price of oil since the beginning of the year. The Canadian Dollar rose all week and has risen from about $.68 to $.78 (a 15% rise) this year against the dollar. On Wednesday the Canadian Central Bank announced that it would keep interest rates were kept at 0.5%. The bank also raised its GDP projection for 2016 from 1.5% to 1.7%. The announcement to keep interest rates at 0.5% was anticipated widely but the surprise GDP upgrade was not and the loonie rose after the announcement.

Precious Metals

Gold and silver rose during the week until the mid week dollar strengthen curbed their rallies. Silver’s price increase over the past week has exceeded gold’s as it plays catch-up to gold which outpaced silver in the first quarter.

Oil

Oil rose to over $41 a barrel on news that Russia and Saudi Arabia reached an agreement to freeze output. Oil’s rally was slowed a bit when OPEC announced that they saw weaker global demand.

Whither Inflation?

Rising oil prices and a declining dollar may act to provide the Fed the inflation it wants in order to justify rate hikes this year. Rising oil price would cause, not just an increase in gas prices, but in finished goods as oil is a major component of the cost of producing goods. As producer prices increase, producers pass those costs on to consumers. A declining dollar will make imports, mainly from China more expensive, adding further upward pressure on consumer prices. Raising rates, however, will do nothing to alleviate the impact of higher prices.

Here are some reports that could impact currency movements next week:

Apr 18 NAHB Housing Market Index Apr

Apr 19 Building Permits Mar

Apr 19 Housing Starts Mar

Apr 20 MBA Mortgage Index 04/16

Apr 20 Existing Home Sales Mar

Apr 20 Crude Inventories 04/16

Apr 21 Initial Claims 04/16

Apr 21 Continuing Claims 04/09

Apr 21 Philadelphia Fed Apr

Apr 21 FHFA Housing Price Index Feb

Apr 21 Natural Gas Inventories 04/16

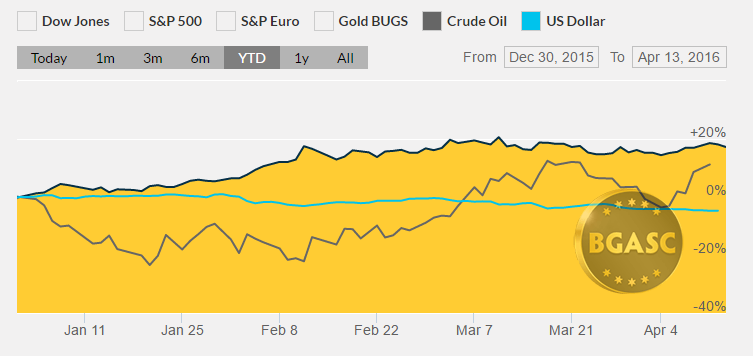

Year to Date Dollar Index, Oil and Gold Prices

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.