FX – Friday Global Currency Review & For Forecast For 4-8-16

A Week Of Uncertain Direction

This week brought a raft of mostly poor economic data that impacted the dollar negatively.

On Tuesday, we learned that U.S. factory orders fell 1.7% in February and that the U.S. trade deficit increased to its highest level in six months as imports exceeded exports. The U.S. trade deficit rose to $47.1 billion, up 2.6 percent from a January’s $45.9 billion deficit. The increase in the trade deficit was concerning because February was a month during which the value of the dollar declined which should have helped U.S. exports. It didn’t.

The decline in factory orders and the widening U.S. trade deficit caused the Bank of America, the Atlanta Fed and other economists to slash their estimates for U.S first quarter GDP to less than 1%.

The Dollar vs the Yen and Euro

The dollar has fallen most of 2016 on the release of mixed to poor economic data and the failure of the Federal Reserve to raise interest rates as had been expected. This week the value of the Japanese Yen reached a 17 month high against the dollar.

Japanese stocks are down 17% this year, but the Yen is strengthening. Japanese Prime Minister Shinzo Abe told the Wall Street Journal earlier this week that Japan would not engage in “arbitrary interventions” to weaken the yen. Ironic that the Prime Minister would speak this way as Japan’s entire fiscal and monetary policies over the past 20+ years have been “arbitrary interventions”!

Indeed, the Bank of Japan’s Governor Haruhiko Kuroda chimed in this week that that he is ready to ease monetary policy further to help the economy.

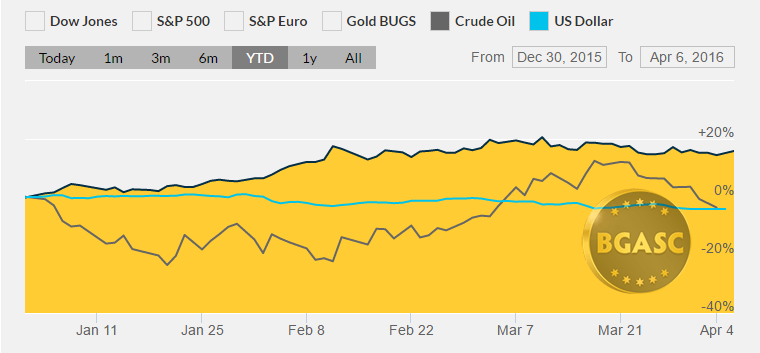

Paradoxically, while the United States Federal Reserve has not raised interest rates this year, the United States doesn’t have negative interest rates and is not engaged in any stimulus program as is Japan. Yet despite having a positive rate of interest and no stimulus, the dollar continues to fall. The Dollar Index* is down about 4.5% this year and has been trading around 94.50 all week.

The Euro has also been on the rise this year despite the European Central Bank lowering interest rates further into negative territory and expanding its stimulus program.

Emerging Markets

Brazil’s Real, a barometer for emerging market currencies, after recovering from last year’s rout of 33% rose about 8% earlier this year is falling again along with the price of oil and other commodities. The Real posted its longest losing streak in three weeks this week.

Gold

Gold has had a volatile week rising and falling over 1% a day in recent trading sessions. After climbing 16% in the first quarter of 2016, gold seems to be taking a breather failing to break out on the high or low ends. Silver is following a similar trading pattern.

Oil

After a major collapse over the past year, the direction of the price of oil remains unclear. Since hitting its lows under $30’s a barrel last month, the price of oil has surged and fallen on talks or rejection of talks of a production freeze among oil producing nations. Also driving oil higher and lower have been the stockpile data releases that show volatile, but elevated inventory levels

Politics

Politics in a Presidential election year have the potential to impact the currency and financial markets.

United States

Second place challengers in the Democratic and Republican Presidential primaries beat their rivals fairly decisively in Wisconsin earlier this week. Bernie Sanders handed Hillary Clinton her sixth defeat in almost as many contests. Mr. Sanders has won six of the last seven primaries or caucuses. Republican Presidential candidate Ted Cruz handily defeated front runner Donald Trump in the Wisconsin primary by about 10 percentage points.

The wins of Messr. Sanders and Trump raise the specter of contested conventions in July. Last April few expected that anyone other than Hillary Clinton would be the Democratic nominee. Ms. Clinton’s email scandal and tepid campaigning have stalled her campaign, making her nomination no longer the shoo-in it was once considered. Her connection to the Panama Papers leak and/or an indictment by the FBI may further dent or dash her chances of getting her party’s nomination.

A year ago, virtually no one could have predicted that Donald Trump and Ted Cruz would be the late primary Republican front runners. A year ago it looked like another Bush/Clinton contest between Jeb and Hillary. Political uncertainty as to who may emerge as each party’s presidential nominee will weigh on the dollar. A Sanders, Cruz or Trump nomination will certainly call in to question the Federal Reserve Members and their re-appointment status.

The direction of U.S. economic, trade and foreign policy will also most likely change if any of the three aforementioned candidates are nominated. Hillary Clinton’s nomination would for better or worse, provide the most continuity to current U.S. fiscal and monetary policies. Uncertainty is not good for any market, including the currency markets. Continued uncertainty as to who might be the nominees for President will continue to apply downward pressure on the dollar.

International

The leak of the Panama Papers has already claimed its first casualty- the Prime Minister of Iceland, who resigned after it was disclosed that he had undisclosed overseas accounts with interests in failed Icelandic banks. The Prime Minister of the United Kingdom David Cameron’s father was also shown to have undisclosed overseas accounts. The Panama Papers may provide issues for David Cameron’s Conservative Party that could weigh further on the British Pound which is already down 2.5% this year on fears of Britain leaving the Eurozone if its citizens vote to do so on June 23rd later this year.

Here are some reports that could impact currency movements next week:

Apr 12 2:00 AM Treasury Budget Mar

Apr 12 8:30 AM Export Prices ex-ag. Mar

Apr 12 8:30 AM Import Prices ex-oil Mar

Apr 13 2:00 AM Fed’s Beige Book Apr

Apr 13 7:00 AM MBA Mortgage Index 04/09

Apr 13 8:30 AM Core PPI Mar

Apr 13 8:30 AM PPI Mar

Apr 13 8:30 AM Retail Sales Mar

Apr 13 8:30 AM Retail Sales ex-auto Mar

Apr 13 10:00 AM Business Inventories Feb

Apr 13 10:30 AM Crude Inventories 04/09

Apr 14 8:30 AM CPI Mar

Apr 14 8:30 AM Core CPI Mar

Apr 14 8:30 AM Initial Claims 04/09

Apr 14 8:30 AM Continuing Claims 04/02

Apr 14 10:30 AM Natural Gas Inventories 04/09

Apr 15 8:30 AM Empire Manufacturing Apr

Apr 15 9:15 AM Capacity Utilization Mar

Apr 15 9:15 AM Industrial Production Mar

Apr 15 4:00 PM Net Long-Term TIC Flows Feb

Year to Date Dollar Index, Oil and Gold Prices

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.