FX Friday Global Currency Review & Forecast For 10-28-16

U.S. 3rd Quarter GDP First Estimate of 2.9% Beats Estimates.

The United States Gross Domestic Product grew at 2.9% in the third quarter, according to the United States Commerce Department. Higher soybean exports and business investment drove the first estimate of US GDP to 2.9% up from 1.4% in the second quarter. The average third quarter GDP estimate was 2.5%.

While GDP components exports and restocking of business inventories were higher than expected, consumer spending rose just 2.1% and investment in business equipment and building supplies were down.

The rise in exports driven by soybeans is not expected to repeat in future quarter as soybean exports benefitted from poor South American harvest this year. Stripping out the one time gain in exports, while factoring in the 2.1% growth in consumer spending and decrease in business and building equipment investment and the GDP number was probably below 2%.

The Dollar Index* reached 99 earlier in the week and spiked on announcement of the higher than expected GDP number, but fell back as traders digested the data behind the top line number. The Dollar Index was at 98.75 in Friday early morning trading. The dollar continues to outperform nearly all other global currencies.

The British Pound remains mired at a 168 year low at $1.21 on “Hard Brexit” fears.The Euro fell to $1.08, its lowest value vs the dollar in eighteen months, on dovish comments by the European Central Bank regarding its monetary policy and the Chines Yuan fell to a five year low.

Dollar strength represents a wild card in the Fed’s deliberations on raising interest rates. A stronger dollar has a deflationary impact as imports become less expensive. Since the United States economy and Gross Domestic Product is based on consumer spending much of it done on foreign imports, a strong dollar curbs inflation.

While the GDP number for the third quarter was better than expected the Dollar Index fell which was probably welcome relief for the Fed. The Fed has long stated that they wish to see inflation near their 2% target. A strong dollar makes that goal harder to achieve and reduce the chanced of an interest rate hike.

Perhaps, a rate hike is already baked into the current currency markets as a majority of market participants now expect a rate hike at the Fed’s December meeting. As the dollar stabilized this week at lofty level, gold and silver managed to eke out small gains.

Economic reports this week did little to change the economic outlook. September new home sales were weaker than expected and the August new home sale data was revised lower. The news cycle continued to be dominated the Presidential Campaign and Wikileaks revelations regarding corruption in the DNC, Clinton campaign and the Clinton Foundation.

Gold and Silver

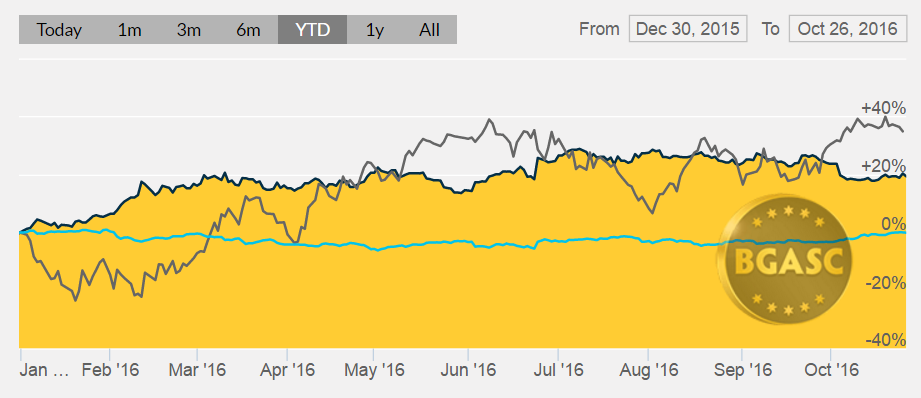

Gold rose this week after being flat last week. Gold traded in a range between $1308-1350 in September, further consolidating it gains from earlier in the year. Gold broke to the upside from the low end of its September trading range following the Fed’s September 20-21 meeting. Gold ended two weeks ago at $1322 an ounce. Gold, however, fell below $1,300 an ounce in the first week of October, dropping $75 an ounce to $1250 an ounce. Gold retraced some of its losses this week.

Gold was trading at $1273 an ounce Friday morning, up $7 from last Friday morning.

Year to Date Dollar Index, Oil and Gold Prices

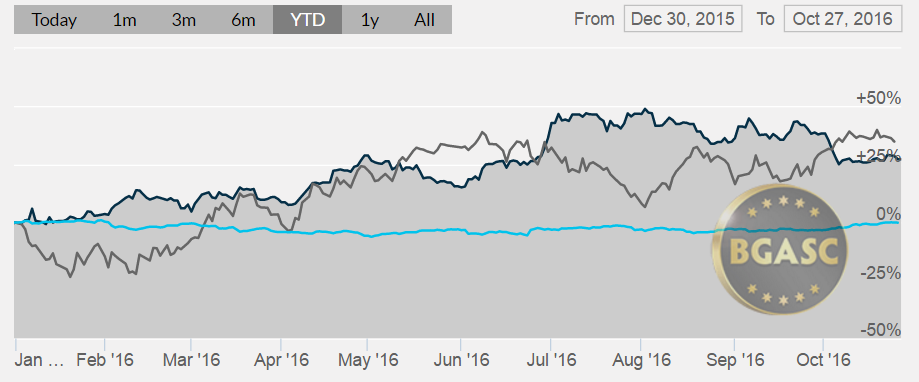

Silver also rose this week after stabilized last week. Silver had risen significantly after the Fed’s September 20-21 meeting at which interest rates were left alone. The 12% losses in silver, erased the post Fed gains and were the worst percentage losses for silver in a week since 2013.

The price of silver Friday morning was at $17.75 an ounce, up $0.26 from last Friday morning.

Year to Date Dollar Index, Oil and Silver Prices

Oil

Oil continues to trade around $50 a barrel on the strength of OPEC’s decision to cut production. Oil rose the first six months of 2016 and levelled off during the summer, trading on news of stockpiles and the possibility of output freeze talks. The OPEC decision to cut output has pushed oil back to over $50 a barrel. Saudi Arabia announced yesterday that it was willing to cut its output by 4%. The announcement help oil maintain its gains of recent weeks.

Year to date, oil is now out-performing gold and silver.

What’s next?

The Presidential campaign continues to capture the attention of market participants with odds heavily favoring Ms. Clinton. To date, daily Wikileaks revelations about Clinton conflict of interests and other unsavory items (largely ignored by the main stream media) have neither landed a knockout blow or influenced the polls.

Next week’s main economic release is the final non farm payroll before the election on November 8. Personal spending for September will also be released. The Fed will have their November meeting on the second of November, but few market participants expect a rate hike to come at that meeting. Seventy percent of market participants surveyed believe, however, that the Fed will raise interest rates at their December meeting. If next week’s non farm payroll surprises to the downside, the chance of a rate hike may lessen.

Here are some economic reports that could impact gold, silver and currency movements next week:

Oct 31 Personal Income Sep

Oct 31 Personal Spending Sep

Oct 31 Core PCE Price Index Sep

Oct 31 Chicago PMI Oct

Nov 1 ISM Index Oct

Nov 1 Construction Spending Sep

Nov 1 Auto Sales Oct

Nov 1 Truck Sales Oct

Nov 2 MBA Mortgage Index 10/29

Nov 2 ADP Employment Change Oct

Nov 2 Crude Inventories 10/29

Nov 2 FOMC Rate Decision Nov

Nov 3 Challenger Job Cuts Oct

Nov 3 Initial Claims 10/29

Nov 3 Continuing Claims 10/22

Nov 3 Productivity-Prel Q3

Nov 3 Factory Orders Sep

Nov 3 ISM Services Oct

Nov 3 Natural Gas Inventories 10/29

Nov 4 Nonfarm Payrolls Oct

Nov 4 Nonfarm Private Payrolls Oct

Nov 4 Hourly Earnings Oct

Nov 4 Unemployment Rate Oct

Nov 4 Average Workweek Oct

Nov 4 Trade Balance Sep

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.