FX Friday Global Currency Review & Forecast For 4-29-16

Commodities and Commodity-Based Currencies Rise as the Dollar Falls

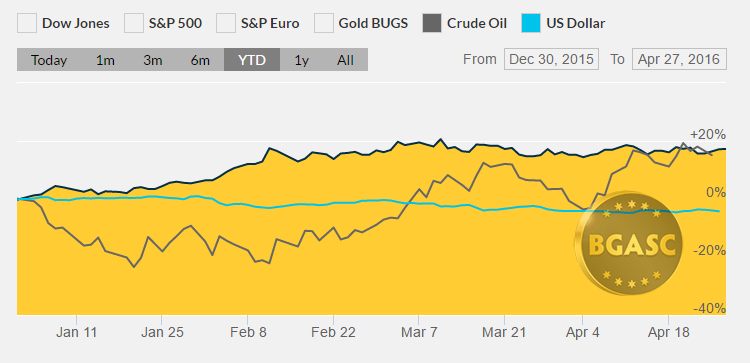

The price of oil has reversed sharply from being down 20% on the year in early February to rising 20% in April. Oil was expected by many market observers to languish for years below $40 a barrel and perhaps drop further in 2016. Oil prices this week, however, have stretched into the $40’s.

Traders anticipated that the dollar would strengthen in 2016, as the Fed was expected to embark on a journey of rate hikes throughout the year, while other central banks cut their benchmark rates. The Fed’s inactivity on the rate hike front and forward guidance that indicated the Fed would proceed cautiously before pulling the trigger on the next rate hike have weakened the dollar. The Fed continued to talk about how gradual rate hikes were appropriate at their meeting this week, but did not raise rates.

Oil

Oil prices topped $45 a barrel this week, a level many analysts thought unattainable for years. The increase in the price of oil this year is remarkable given no production freeze has been agreed and the prospects for one have been dashed by Saudi Arabia. In addition, Kuwait announced it would boost its oil output by June. Oil is up about 20% year this month alone (see chart below).

Canadian Dollar

The Canadian Dollar, whose value is closely tied to the price of oil, continued to rise this week. The Canadian Dollar rose to its highest level since July 2015 and hit nearly $.80 to the U.S. Dollar.

Russian Rouble

Russia’s economy is very closely tied to the price of oil. According to the World Bank, oil is by far Russia’s largest export and represents about 15-20% of Russia’s GDP and the majority of government revenues. The Rouble has risen about 3% this month, a pace lower than the near 20% increase in the price of oil over the same time period.

The Dollar

The dollar has suffered all year from Fed back pedaling from their normalization of interest rate policy. Markets understood that once the Fed finally raised interest rates for the first time in ten years in December 2015, that it would begin a process of raising rates gradually over the coming 3-5 years. Instead, the Fed has not raised interest rates at all in 2016 and has reduced expectations for the number of rate hikes that may be coming in 2016 to just two. This dynamic has driven the Dollar Index* down under 95.

U.S. economic data this week was not encouraging. Durable goods were up only slightly in March after falling -3.1% in February. Non defense durable goods were flat. Consumer Confidence also declined in March from a reading of 96.1 to 94.2. Home prices as measured by the Case-Shiller 20-City Home Prices rose 5.38% Y/Y but were lower than the 5.50% Y/Y estimate.

The Fed would like to raise rates as the economy strengthens, not weakens. If the economy continues to weaken but prices rise due to a falling dollar and rising commodity prices, the Fed may have no choice but to raise rates.

British Pound

The British Pound rose this week, despite reports of slowing growth. The Pound rose because recent polls show the “stay” in Europe vote scheduled for June is increasing. Currency traders believe a “Brexit” would be negative for the Pound so any news that the leave Europe initiative may be defeated causes an uptick in the value of the Pound.

Japanese Yen

The Yen retreated this week after advancing in recent weeks. The decline in the Yen was driven by The Bank of Japan’s contemplation of stimulus expansion and negative interest rates on lending to banks.

Gold

The price of gold stabilized during the week and traded in a tight range.

Silver

Silver rose dramatically last week but failed to close about $17 an ounce, peeked above that mark earlier this week.

What’s next?

Rising oil and commodity prices and a declining dollar may provide the Fed with the inflation they so desperately wish to create. Higher oil and commodity prices will directly create higher consumer prices for food, gas, heating oil and other finished goods. A weaker dollar will cause imports, which make up a large portion of consumer goods in the U.S., to become more expensive. The Fed has said they want to see improvements in the economy, labor market and inflation as they “proceed cautiously” before raising interest rates again. Higher inflation readings and higher interest rates may be just around the corner if oil continues its ascent and the dollar continues to weaken.

Here are some reports that could impact currency movements next week:

May 2 ISM Index Apr

May 2 Construction Spending Mar

May 3 Auto Sales Apr

May 3 Truck Sales Apr

May 4 MBA Mortgage Index 04/30

May 4 ADP Employment Change Apr

May 4 Productivity-Prel Q1

May 4 Unit Labor Costs – Prel Q1

May 4 Trade Balance Mar

May 4 Factory Orders Mar

May 4 ISM Services Apr

May 4 Crude Inventories 04/30

May 5 Challenger Job Cuts Apr

May 5 Initial Claims 04/30

May 5 Continuing Claims 04/23

May 5 Natural Gas Inventories 04/30

May 6 Nonfarm Payrolls Apr

May 6 Nonfarm Private PayrollsApr

May 6 Unemployment Rate Apr

May 6 Hourly Earnings Apr

May 6 Average Workweek Apr

May 6 Consumer Credit Mar

Year to Data Dollar Index, Oil and Gold Prices

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.