FX Friday Global Currency Review & Forecast For 5-13-16

Dollar Strength Follow Through Fades

The U.S. Dollar

Last week the Dollar Index* rose as two Fed Presidents (Messrs. Lockhart and Williams) raised the specter of a rate hike at the Fed’s June meeting. A rate hike in June was something that most market participants thought was off the table.

Earlier this week, in what seemed to be an obvious attempt to boost the dollar further, two more Fed Presidents, Messrs. Evans and Kashkari, made statements about the possibility of a rate hike in June. It didn’t work this week. Neither Fed President gave a glowing diagnosis of the U.S. economy, but made sure they added language to their statements that a rate hike might be possible at the Fed’s June meeting. The dollar rally had faded by Wednesday.

Instead of talking about a rate hike, it appears that the market needs to see at least one rate hike before it will believe that the reduced Fed guidance of two rate hikes in 2016 (down from four hikes) in a possibility. The Dollar Index is acting as if there won’t be ANY rate hikes in 2016.

The Dollar Index rose from under 93 last week to over 94 by the end of the week and opened this week around 94. In early week trading the Dollar Index continued to rise but gave up all of the week’s gains on Wednesday falling below 94 again.

Trump On Restructuring U.S. Debt

Donald Trump made some comments on Monday regarding a solutions to solving the U.S. debt issue that should have impacted the dollar but did not. Mr. Trump suggested in an interview with CNN that the U.S. could print the money to pay off its debts. He told CNBC last week that the U.S. could also renegotiate the terms of U.S. debt. Either of Trump’s proposed actions would almost certainly harm the dollar. On Monday, however Mr. Trump backed away from his “renegotiation of the national debt” comments. The markets did not react to any of Mr. Trump’s statements on the debt and the Dollar Index ended Monday higher.

Puerto Rico’s Debt Crisis

It also became clear this week that Puerto Rico would have to restructure its $70 billion in bond debt, a path that Treasury Secretary Jack Lew favors over a bailout. The news on Puerto Rico’s debt also did not have an immediate impact on the dollar.

It may take time for the markets to digest Mr. Trump’s comments and the Puerto Rican debt situation which are clearly dollar negative mid and longer term.

Most currencies fell early in the week on dollar strength but rebounded by mid-week as the dollar rally stalled.

The Japanese Yen

The Japanese Yen tumbled from an 18 month high earlier in the week on intervention warnings from Japan’s finance minister. Yet the Yen rebounded by mid-week against the dollar.

The British Pound

The British Pound continued to fall in advance of June’s Brexit vote. Polls are showing a “leave” vote is still a possibility. That potential has put downward pressure on the pound all year. The pound, however, also rebounded mid week on dollar weakness.

Gold and Silver

Gold and silver pulled back early in the week, with silver getting the hardest hit, falling over 3% and dipping below $17 an ounce earlier in the week. Gold and silver bounced back to recoup half of their losses by mid week.

Oil

Oil seems to have consolidated its gains over $40 a barrel. While 3% intraday price swings have been common the past two weeks, they occur at prices over $40 a barrel. Most recently, oil rose to over $46 a barrel on a report that U.S. crude oil stockpiles declined for the first time since March.

What’s next?

Next week’s consumer price index reading may provide some clues as to whether the Fed might raise interest rates at its June meeting. A reading over .03% may put a rate hike in play. Anything lower would weigh in favor of a ‘wait and see’ approach. Weekly jobless claims normally do not factor into Fed decision making as they tend to look at longer term jobless claim data. A high number next week, however, may give the Fed pause as this week’s jobless claims number was higher than expected. If there is a higher than expected number next week, a trend could be developing.

Important housing and industrial production reports are also on tap next week. Weakness in either of those reports could scuttle talk of a Fed rate hike in June.

Here are some reports that could impact currency movements next week:

May 16 Net Long-Term TIC Flows Mar

May 16 Empire Manufacturing May

May 16 NAHB Housing Market Index May

May 17 CPI Apr

May 17 Core CPI Apr

May 17 Housing Starts Apr

May 17 Building Permits Apr

May 17 Industrial Production Apr

May 17 Capacity Utilization Apr

May 18 MBA Mortgage Index 05/14

May 18 Crude Inventories 05/14

May 18 FOMC Minutes Apr 27

May 19 Initial Claims 05/14

May 19 Continuing Claims 05/07

May 19 Philadelphia Fed May

May 19 Natural Gas Inventories 05/14

May 20 Existing Home Sales Apr

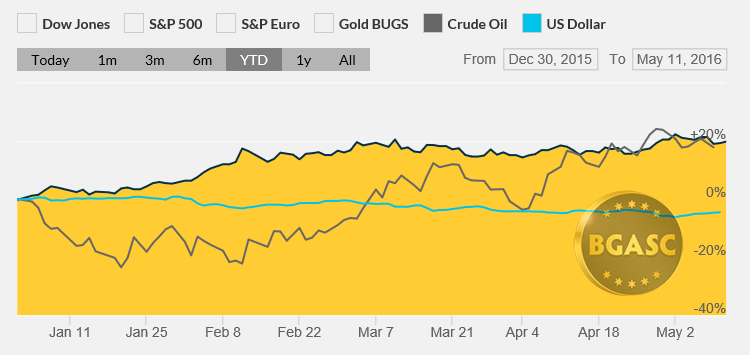

Year to Date Dollar Index, Oil and Gold Prices

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.