FX Friday Global Currency Review & Forecast For 5-27-16

Fed Presidents Roar- RATE HIKES ARE COMING!

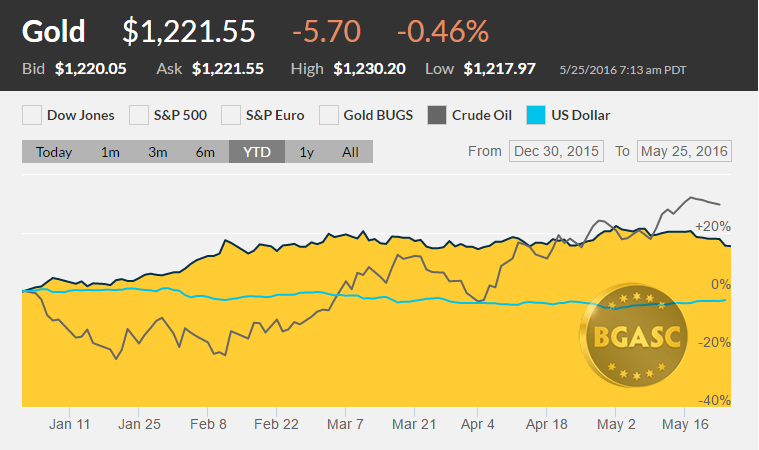

For the third week in a row we’ve heard a series of calls by Fed Presidents for rate hikes in 2016. The incessant barrage of Fed Presidents arguing for rate hikes, most of them non voting members, has had its impact. In early May, the Dollar Index* had fallen from about 95 to 92. The Dollar Index was falling because earlier in the year the Fed had struck a dovish stance and reduced their call for the number of rate hikes in 2016 from four to two. The market expectations for two rates hikes were discounted to a point in late April where many market observers believed rate hikes would not come at all in 2016.

Then the rate hike talk began in earnest. One after the other, starting in early May, Fed Presidents Rosengren, Lacker, Lockhart, Dudley, Kapan, Williams and Harker reminded markets that a rate hike was possible as early as the next meeting and that a series of rate hikes of, perhaps two or three, were most likely coming. A few Fed Presidents used the expression “June is a Live Meeting” to drive home the point. Some of the Fed Presidents repeated their rate hike prognostications two or three times over the past two weeks.

Most Fed Presidents cited “labor market strength” as a factor in their rate hike chatter.

The markets got the message. The repeated rate hike mantra sunk in. The Dollar Index rose from 92 at the beginning of May to over 95.50 this week. Gold and silver lost a good portion of their value during the Fed President rate hike onslaught. Before the rate hike chatter offensive, a rate hike in June was considered to be close to ‘no chance’. After the Fed chatter it was starting to seem almost probable. Indeed, the rate hike talk was so effective, perhaps too effective, that St. Louis Fed President James Bullard had to assure markets this week that a June rate hike was not a done deal.

The Fed has learned to conduct monetary policy through words, not actions. Having conditioned markets to expect rate hikes, the Fed will either have to conduct a series of rate hikes or find convenient excuses (e.g. worse than expected incoming data, Brexit, political or global uncertainty) not to.

Other Currencies

During the dollar ascent the past two week, other currencies fell vs. the dollar. The dollar rose against the Canadian Dollar and the Euro but fell against a strengthening Japanese Yen.

Oil

Oil touched $50 a barrel this week and is up nearly 25% year to date, out performing nearly all commodities, including gold.

Gold and Silver

Gold and silver are off from their early May highs of about $1280 and $17.60 an ounce, respectively. Gold traded in the $1218-20’s range this week, while silver traded as low as $16.15 an ounce.

Year to Date Dollar Index, Oil and Gold Prices

What’s next?

By putting rate hikes back in play, attention will be focused on the June and July Fed meetings. The June Fed two day meeting ends on June 15 followed by a press conference. If rates are not raised at that meeting, the press conference should provide clues as to the whether the Fed will raise rates at July’s meeting after which there is no scheduled press conference.

Federal Reserve Chair, Janet Yellen speaks June 6. The Brexit vote is June 23.

After the Fed’s July meeting we should have some clarity on the Fed’s position on 2016 rate hikes, but then we will enter the uncertainty of the Presidential election season.

Since the Fed has focused on the labor market as a primary consideration in deciding whether to raise rates, next week’s initial jobless claims and non farm payroll numbers will be the most closely watched reports on the calendar.

Here are some reports that could impact currency movements next week:

May 31 Personal Income Apr

May 31 Personal Spending Apr

May 31 PCE Prices Apr

May 31 Case-Shiller Index Mar

May 31 Chicago PMI May

May 31 Consumer Confidence May

Jun 1 MBA Mortgage Index 05/28

Jun 1 Construction Spending Apr

Jun 1 ISM Index May

Jun 1 Crude Inventories 05/28

Jun 1 Auto Sales May

Jun 1 Truck Sales May

Jun 1 Fed’s Beige Book Jun

Jun 2 Challenger Job Cuts May

Jun 2 ADP Employment Change May

Jun 2 Initial Claims 05/28

Jun 2 Continuing Claims 05/21

Jun 2 Natural Gas Inventories 05/28

Jun 3 Nonfarm Payrolls May

Jun 3 Nonfarm Private May

Jun 3 Unemployment Rate May

Jun 3 Hourly Earnings May

Jun 3 Average Workweek May

Jun 3 Trade Balance Apr

Jun 3 Factory Orders Apr

Jun 3 ISM Services May

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.