FX Friday Global Currency Review & Forecast For 5-6-16

The Dollar Rebounds On Fed Rate Hike Chatter

It was bound to happen. U.S. economic data was not encouraging. The Dollar Index* was falling almost in a straight free fall from 95 to 92.50 in just a week. Then, as if on queue, on Tuesday, out came the Fed Presidents talking about how a rate hike in June might happen.

Atlanta Fed President Dennis Lockhart spoke earlier this week and tossed out all the typical Fed “hawkish” buzz words. June, he prounced, would be a “live” meeting. He added a rate hike at the next Fed meeting was a “real possibility”. Of course, he added the normal Fed caveat that something could happen to change the direction towards a rate hike in June. The excuse Mr. Lockhart gave was if Great Britain voted to leave the European Union in June. A Brexit would fall under the Fed’s catchall “global uncertainty” as a reason to be cautious in considering whether to raise rates.

Adding to Mr. Lockhart’s rate hike chatter this week was San Francisco President John Williams. Mr Williams stated he too would be in favor of a rate hike in June, if the economy continues along the same trajectory. Mr. Williams brushed aside the 0.5% GDP growth in the first quarter by saying he doesn’t take the poor growth reading as a “strong signal”. Mr. Williams said he remains optimistic about the U.S. economy and still expects 2% GDP growth in 2016. Then he added “a lot can happen between now and the middle of June” (the Fed meeting is scheduled for June 14-15) and if the economic data comes in weaker than expected he would argue to hold off on rate hikes.

The re injection of imminent rate hikes possibility back into the Fed narrative was enough to set the dollar rallying. The Dollar Index bounced off its 92.50 low on Tuesday and soared past 93 on Tuesday and Wednesday. The dollar rallied despite ADP payrolls coming in far lower than expected on Wednesday and a decline in U.S. worker productivity.

As the dollar rose, other currencies faded.

Australian dollar

The Australian dollar got clobbered on Tuesday when its central bank, the Reserve Bank of Australia announced a suprise rate cut. The RBA rate cut of .25% brought rates to an all time low of 1.75%.

The Chinese Yuan

China devauled the Yuan mid week by the most in eight months driving the Yuan down against the dollar to an eight day low.

Russian Rouble

The Russian Rouble had been rising all year on improving oil prices. On Wednesday, the Rouble took a hit of nearly 3%, its biggest decline since early February as oil prices retreated on supply glut concerns. The Rouble is still up nearly 10% on the year.

The Euro

The Euro has been rising against the dollar all year and hit an eight month high of $1.15 against the dollar on Tuesday. The Euro got a boost from better than expected Euro-zone industrial production numbers released earlier in the week. The Euro fell back on dollar strength on Wednesday in the aftermath of the Fed Presidents talking about rate hikes.

The Yen

The Yen rose last week when the Bank of Japan held off on further stimulus and rate cuts. The Yen fell this week on dollar strength and statements from the Bank of Japan that indicated they might intervene to stop the Yen from rising.

The British Pound

The British Pound continues to trade almost exclusively on polls that indicate the direction that United Kingdom voters may take when they go to the polls in June to vote whether to stay in the European Union. An indication that a “stay” vote is leading in the polls strengthens the Pound, a “leave” vote weakens it.

Gold and Silver

Gold and silver began the week sharply higher but pulled back after Tuesday’s Fed President rate hike chatter. Both metals appear to be taking a breather after running up over 20% so far this year.

Oil

Oil, like gold and silver and other commodities has traded higher all year. Oil now trades on news of production numbers and potential meetings of oil producers where they might freeze production. Oil remains above $40 a barrel.

What’s next?

Today’s Non Farm Payroll number will be closely watched. Anything under 200,000 new jobs created may cause the Fed to call off their June rate hike. A number higher than 200,000 may put rate hikes back on the table subject to next week’s inflation numbers. The Producer Price Indexes will be released next week and the Consumer Price Index the following week. If the inflation numbers remain low, the Fed may hold off on raising rates in June even if the Non Farm Payroll number tops 200,000.

Here are some reports that could impact currency movements next week:

May 10 10:00 AM JOLTS – Job Openings Mar

May 10 10:00 AM Wholesale Inventories Mar

May 11 7:00 AM MBA Mortgage Index 05/07

May 11 10:30 AM Crude Inventories 05/07

May 11 2:00 PM Treasury Budget Apr

May 12 8:30 AM Initial Claims 05/07

May 12 8:30 AM Continuing Claims 04/30

May 12 8:30 AM Import Prices ex-oil Apr

May 12 8:30 AM Export Prices ex-ag. Apr

May 12 10:30 AM Natural Gas Inventories 05/07

May 13 8:30 AM PPI Apr

May 13 8:30 AM Core PPIApr

May 13 8:30 AM Retail Sales Apr

May 13 8:30 AM Retail Sales ex-auto Apr

May 13 10:00 AM Business Inventories Mar

May 13 10:00 AM Mich Sentiment May

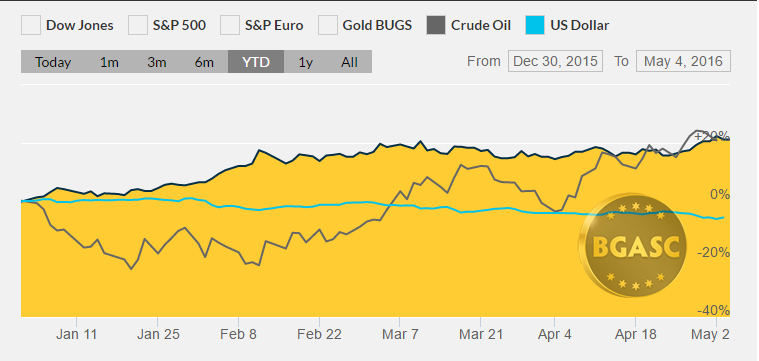

Year to Date Dollar Index, Oil and Gold Prices

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.