FX Friday Global Currency Review & Forecast For 9-09-16

Fed insists Rate Hike Still On the Table Despite Recent Poor Jobs and Economic Reports

The Fed reappeared on market participants’ radar screens last month when a few Fed Presidents revived the idea that a rate hike was possible in September. Janet Yellen confirmed that possibility at her Jackson Hole speech later in August. Fed Vice Chair reaffirmed that Ms. Yellen’s remarks at Jackson Hole were indeed consistent with the possibility of a rate hike in September. The Vice Chair was careful to note that the upcoming August Non Farm Payroll Report would be an important factor in determining the direction of rate hikes.

Last Friday, the widely anticipated Non Farm Payroll number was released and it was a big miss, just 150,000 new jobs were created in August vs. expectations ranging from 180-200K. Market participants took this poor job reading as a sign that a rate hike in September was off the table.

Then, as if on cue Fed Presidents Williams, earlier this week and Rosengren today expressed their support for interest rate hikes. San Francisco Fed President John Williams insisted the “economy was strong” and rate hikes were warranted. Boston Fed President Eric Rosengren warned that the economy risked overheating if rates were not raised. These statements about the health of the economy contradict not only the sub par August non farm payroll reading but also declines in the ISM manufacturing and services reports. The ISM services report reflected a declining barely expanding sector and the manufacturing report indicated a contraction.

If market participants discount the Fed’s calls for rate hikes and the Dollar Index* falls, Fed officials feel obliged to remind market participants that the Fed is still relevant and can raise interest rates as soon as the next meeting.

The next Fed meeting takes place on September 20-21. We expect the Fed to continue to remind market participants that a rate hike is a possibility at that meeting. Current surveys, however show that upwards of 65% of market participants don’t expect the Fed to move on rate hikes at their September meeting.

Gold and Silver

Gold fell in August after rising most of the year. After last Friday’s job report, gold snapped back and extended its gains on Monday. Gold Reached $1348 an ounce earlier this week but has been beaten back about $15 an ounce by Fed rate hike talk. Recent set backs in the price of gold have been short lived, but the period between now and the September 20-21 Fed meeting may weigh further on gold.

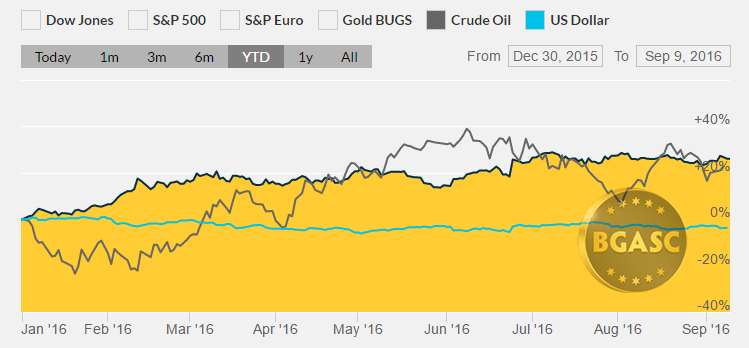

Year to Date Dollar Index, Oil and Gold Prices

Silver popped after the August job report on Friday and hit over $20 an ounce earlier this week. Profit taking and rate hike talk has pushed silver down below $19.50 an ounce this morning. Silver continues to be the best performing asset in 2016, rising well over 40% in 2016. The price of silver is at its highest levels in two years, but far below its all time higher of $50 an ounce reached in April 2011. The price action this week in silver highlights that when precious metals price rise, silver rises it generally rises more than gold.

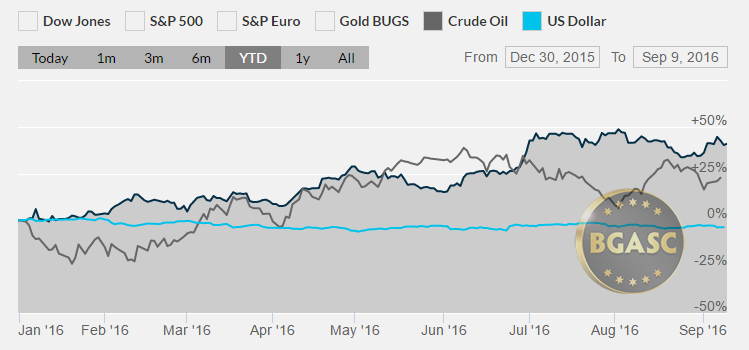

Year to Date Dollar Index, Oil and Silver Prices

British Pound

The British Pound remains mired in the $1.30 area after showing some signs of life recently as the predictions of gloom and doom after the Brexit vote have yet to materialize. Positive economic readings post Brexit have given the pound a boost in recent weeks. The British Pound hit a three week high earlier this week, touching $1.34 on September 7 after having been on a downward trajectory ever since the Brexit vote. The British Pound reached its high of the year at around $1.50 prior to the Brexit vote then fell to around $1.30 after the vote and had remained depressed due to nagging fears of the implications of Brexit and the reduction of interest rates by the Bank of England.

Oil

Oil shot higher in the first six months of 2016. Since then oil has been trading on news of stockpiles and the possibility of output freeze talks. Oil, like gold has been stuck in a trading range and off its highs the past month. Oil continues to spike and fall on inventory reports and from talks about upcoming meetings among oil producers to discuss output freezes. The former depresses prices and the latter boosts them.

What’s next?

The Fed has managed to make it the focus of attention leading up to its meeting later this month. The economic calendar between now and the September 20-21 meeting includes reports on retail sales and inflation numbers that may influence the Fed’s interest rate policy making decisions.

Here are some economic reports that could impact gold, silver and currency movements next week:

Sep 13 Treasury Budget Aug

Sep 14 MBA Mortgage Index 09/10

Sep 14 Export Prices ex-ag. Aug

Sep 14 Import Prices ex-oil Aug

Sep 14 Crude Inventories 09/10

Sep 15 Initial Claims 09/10

Sep 15 Continuing Claims 09/03

Sep 15 Retail Sales Aug

Sep 15 Retail Sales ex-auto Aug

Sep 15 PPI Aug

Sep 15 Core PPI Aug

Sep 15 Philadelphia Fed Sep

Sep 15 Current Account Balance Q2

Sep 15 Empire Manufacturing Sep

Sep 15 Capacity Utilization Aug

Sep 15 Business Inventories Jul

Sep 15 Natural Gas Inventories 09/10

Sep 16 CPI Aug

Sep 16 Core CPI Aug

Sep 16 Mich Sentiment Sep

Sep 16 Net Long-Term TIC Flows Jul

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.