FX Friday Global Currency Review & Forecast For 9-23-16

Fed Gives Up the Spotlight.

The Fed’s September open market committee meeting on September 20-21 came and went without an interest rate hike. All year the Fed has managed to remain the focus of market participants’ attention with incessant threats to raise interest rate. Having cried wolf yet again, perhaps the only thing that will capture market participants’ attention would be an actual rate hike.

The market focus between now and the next Fed meeting in November will be on the Presidential election between Hillary Clinton and Donald Trump. Economic data will be released and if any of it is good, Fed official will be certain to renew their calls for a rate hike or hikes in 2016. The Fed statement following the September meeting indicated that all was well with the U.S. economy other than perhaps a slow down in business inflation and a lack of rising prices. Any improvement in those two sets of data will be raise the possibility of at least interest rate chatter from the Fed.

Markets will also be on alert for an shocks that may come from the European banking sector where German and Italian banks, Deutsche Bank and Banca Monte dei Paschi di Siena attempt to plow through financial difficulties without need for massive central bank intervention.

The Dollar Index* received a boost from the constant Fed rate hike chatter that renewed in earnest in early August and continued through this month. The Dollar Index fell to about 95.50 after the Fed announcement that there would be no interest rate hike following the September meeting but still remains well above the low 94 range in early August. European banking troubles may act to boost the Dollar Index in lieu of a rate hike.

The vast majority of surveyed market participants do not expect a rate hike at the November meeting. Market participants are mixed regarding the possibility of a rate hike at the Fed’s December meeting.

Gold and Silver

Gold rose immediately prior to and after the Fed September meeting. Gold has traded in a range between $1308-1350 in September, further consolidating it gains from earlier in the year. Gold has held, however, above $1300 an ounce all of August and September. Gold broke to the upside from the low end of its September trading range following the Fed’s September 20-21 meeting as was trading at $1338 an ounce Friday morning.

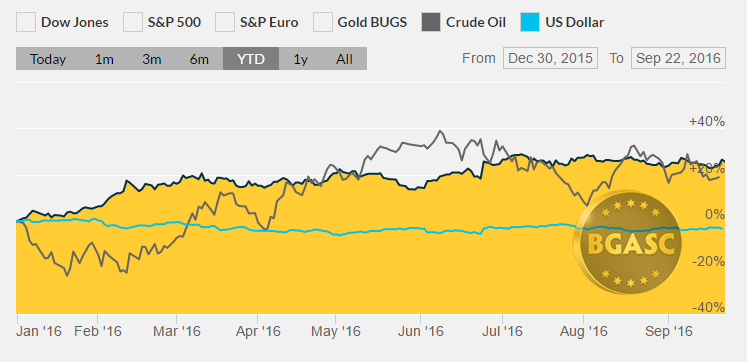

Year to Date Dollar Index, Oil and Gold Prices

Silver also popped after the September Fed meeting and touched briefly over $20 an ounce on Thursday. Profit taking and rate hike talk had pushed silver down below $19.00 an ounce last week. Silver continues to be the best performing asset in 2016, rising well over 40% in 2016. The price of silver is at its highest levels in two years, but far below its all time higher of $50 an ounce reached in April 2011.

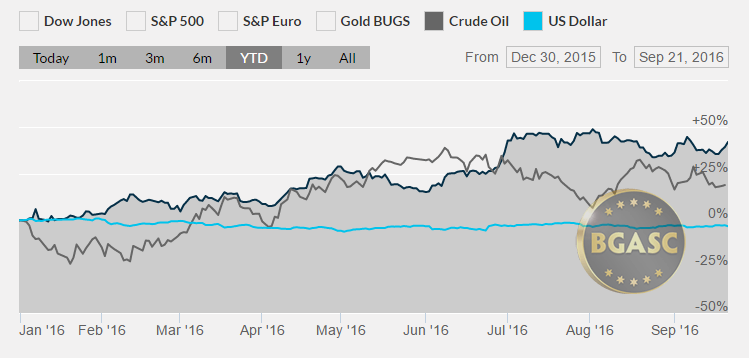

Year to Date Dollar Index, Oil and Silver Prices

British Pound

The British Pound continues to meet resistance at around $1.34. The Pound bounced and fell again this week and remains mired in the $1.30 area. The British Pound has yet to sustain a rally from its post Brexit lows even though the economic gloom and doom predicted by a Brexit vote have not materialized.

Oil

Oil shot higher in the first six months of 2016. Since then oil has been trading on news of stockpiles and the possibility of output freeze talks. This week Russia noted that its output his all time highs. The price of oil continues to spike and fall on inventory reports and from talks about upcoming meetings among oil producers to discuss output freezes. Russia noted that it could reduce output, but indicated that OPEC was unlikely to push for any such reduction in oil output. Oil, like gold has been stuck in a trading range and off its highs the past month. The former depresses prices and the latter boosts them. Oil was trading at $46.19 a barrel on Friday.

What’s next?

The durable goods number next week will provide some insight into levels of business spending. The third estimate of US GDP, unless it varies greatly from the first two estimates, is likely to be a non-event. The Presidential debate on Monday may provide some insight into whom might be elected President and give markets time to digest the impact on financial markets that either a Clinton or Trump Presidency might bring.

Here are some economic reports that could impact gold, silver and currency movements next week:

Sep 26 New Home Sales Aug

Sep 27 Case-Shiller 20-city Index Jul

Sep 27 Consumer Confidence Sep

Sep 28 MBA Mortgage Index 09/24

Sep 28 Durable Orders Aug

Sep 28 Durable Orders, Ex-Transportation Aug

Sep 28 Crude Inventories 09/24

Sep 29 GDP – Third Estimate Q2

Sep 29 GDP Deflator – Third Estimate Q2

Sep 29 Initial Claims 09/24

Sep 29 Continuing Claims 09/17

Sep 29 International Trade in Goods Aug

Sep 29 Pending Home Sales Aug

Sep 29 Natural Gas Inventories 09/24

Sep 30 Personal Income Aug

Sep 30 Personal Spending Aug

Sep 30 Core PCE Prices Aug

Sep 30 Chicago PMI Sep

Sep 30 Michigan Sentiment – Final

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.