Gold to Get a Boost? Global Currency Review & Forecast For 4/13/2018

Syria, Trade Wars & Budget Deficits Boost Gold

Spotlight off the Fed

For the first time in recent years, the Federal Reserve’s monetary policy has not been one of the main drivers of the foreign exchange, equity and precious metals markets. In November 2008, the Federal Reserve first embarked on a $4.5 trillion series of three quantitative easing (QE) programs that lasted until October 2014. During that time period, all eyes were on the Fed as market observers would speculate how long the current quantitative easing program might last, how large it might be and when the next one might begin. The direction of the Dollar Index*, the price of gold and silver and equity markets were largely driven by the Fed’s monetary policy and what Fed officials might say about ending QE and the direction of interest rates.

From the end of QE in October 2014 (and well before that) until December 2015, the Fed threatened to raise interest rates from zero but did not do so until 2015 and then only by a quarter of a percentage point. From December 2015 to December 2016 the Fed again threatened on many occasions to raise interest rates several times during that period but ended up only raising them once in December 2016, again just one quarter of a percentage point.

Having talked about raising interest rates several times a year from 2014-2016 but only raising them once in each of 2015 and 2016, the Fed finally strung together three quarter point interest rates hikes in 2017 (in March, June and December). The Fed also raised interest rates a quarter of a point in 2018 in March. For the past 12-16 months or so markets have seemed less concerned about the direction of Fed interest rate policy and more concerned about the changing economic landscape since Donald Trump became President in January 2017.

Spotlight on Trump Presidency, Trade Wars, International Affairs and Fiscal Policy

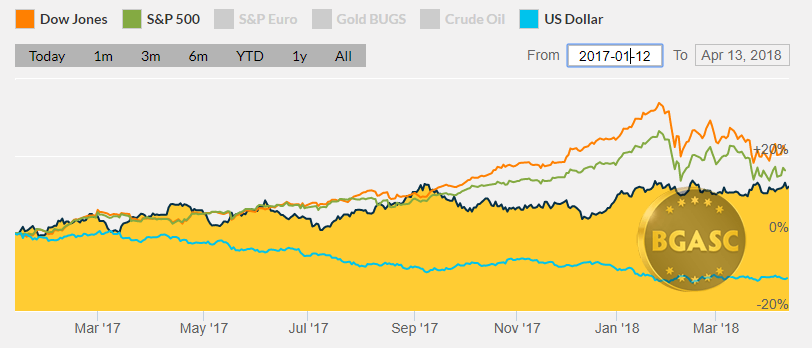

Since President Trump assumed the Presidency the equity markets have been on a tear, with the Dow Jones industrial average rising about 33% from January 2017 to the end of January 2018. The Dow Jones and S&P 500 have fall since the end of January but remain at elevated levels.

Equity prices have risen largely on the anticipation and realization of tax cuts that Trump had promised and on the anticipation but yet to be realized infrastructure spending that would also boost the economy.

In March 2018 President Trump announced his intention to place tariffs on Chinese and other foreign imports. In April 2018 President Trump was discussing possible military action in Syria. The fear of a widening trade and/or hot war has dampened enthusiasm for equities in recent months.

Gold and Silver

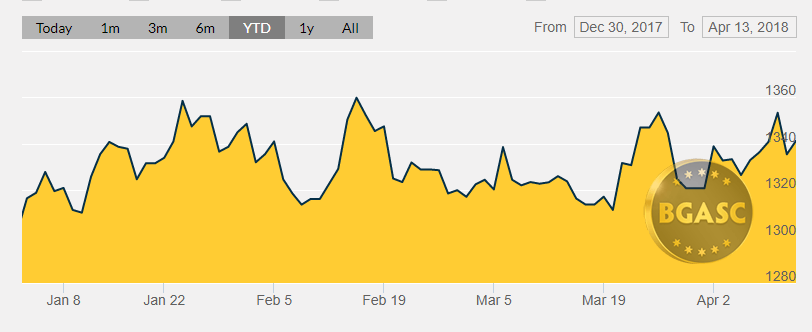

Gold has risen from around $1200 since 2017 to over $1346 as of April 2018, undeterred by four interest rate hikes during that time period. Gold has risen due to a variety of factors including the lower Dollar Index, tax cuts (with no spending cuts) that are perceived to most likely add to the deficit and recently due to the threat of war with Syria and/or lengthy trade wars.

Gold Price Year to Date

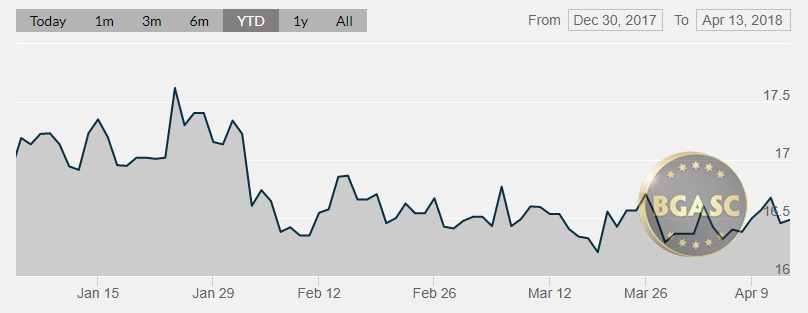

Silver Price Year to Date

Silver, since January 2017 has been flat, opening 2017 around $16.45 and closing April 23 at $16.45. Silver had been one the best performing assets in 2016, rising nearly 20%, at one point topping over $20 an ounce in July 2016. The price of silver has languished in 2017. While industrial demand for silver rose about 4% in 2017, investment demand for silver coins and bars fell about 27%.

Up till now, gold has been receiving the lion’s share of safe haven precious metals investors’ dollars and rising at a faster pace than silver. Generally, however, this is the pattern of a gold bull market. Gold moves first and once gold establishes a sustained bull market, silver starts to move higher. Because silver is a much smaller market, additional safe haven capital flowing into the silver market tends to have a greater positive impact on price.

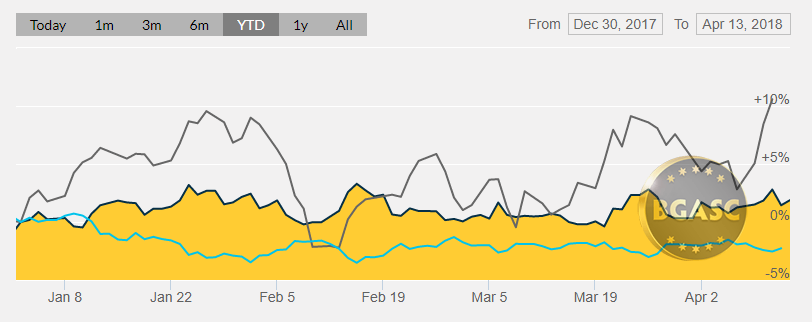

Year to Date Dollar Index, Oil and Gold Prices

The Dollar Index

When the first quantitative easing was launched the Dollar Index was in the low 70’s. During the entire time of QE the Dollar Index stayed within a range between the low 70’s and upper 80’s. The Dollar would drop as each successive QE grew in amount and time and would rise when each QE ended. The Dollar Index soared higher at the end of QE and rose from mid 80’s in the fall of 2014 to over 103 in December 2016. When Donald Trump took office in January of 2017, the Dollar Index

The same factors that drove equity prices higher (tax cuts and expectation of infrastructure spending) have harmed the dollar as concerns over a ballooning deficit were not offset by rising interest rates.

Oil

Oil has been, like gold a superstar performer in 2018, rising over 10%. The price of oil has risen despite record U.S. shale oil production. Rising U.S. oil production has been offset by OPEC production curbs. Oil, however, has risen in recent months largely on the “risk premium” due to geopolitical events that may result in supply disruptions.

Chinese Yuan

The Chinese Yuan reached a multi-year low vs. the dollar in December 2016 of 6.96. Since then, the Yuan has been set stronger vs. the dollar and has been hovering around 6.30 all through 2018. In response to trade tariffs, Chinese officials have stated that they will neither devalue the Yuan, nor dump U.S. Treasuries.

Euro

The Euro has been the main beneficiary of dollar weakness in 2018, in spite of continued bond buying (QE) by the European Central Bank and sustained zero interest rates, rising from around $1.20 in January to around $1.24 in April. The Euro has been rising vs the dollar since January 2017. The Euro hit a multi-year low in December 2016 of around $1.04.

British Pound

Ever since the Brexit vote in June 2016 the British pound has suffered. The British Pound reached a high of the that year at around $1.50 prior to the Brexit vote then fell to around $1.30 after the vote and bottomed in March of 2017 around $1.22. Since then, the Pound has risen steadily to $1.42 as an economic collapse that was feared following the Brexit vote has not materialized. The Pound remains vulnerable to the timeline of Brexit and it terms which have yet to be settled.

Japanese Yen

The Japanese Yen has fallen steadily against the dollar since January 2017. Last week, however, the Yen rose on “safe haven” bids due to the threat of a western allied war with Syria and reached a two month high.

What’s next?

Next week may provide clarity on whether war will erupt in Syria. In addition, there may be further developments in the Chinese US trade situation. Earlier today, Trump declined to name China a currency manipulator. The 2018 mid- term elections will also start to factor into the markets’ thinking. If Democrats gain control of the House and Senate, the prospect of impeachment of Donald Trump may rattle the equity markets and the dollar and boost gold and silver. In addition, prominent Democrats have openly discussed repealing the Trump tax cuts if they wrest control in November.

* The US Dollar Index tracks the US dollar vs. the Euro, the Japanese Yen, the British Pound, the Canadian Dollar, the Swedish Krona and the Swiss Franc. The Euro comprises nearly 58% of the index.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.