Will Fear or Greed Prevail During the Trump Administration?

Trump’s First 100 Days Provide Positive Jolt to the Markets

Before the 2016 Presidential election, conventional wisdom was that a Trump win would be a disaster for the financial markets. Mr. Trump’s mercurial and unpredictable personality, market participants believed, would roil the status quo and the markets. Indeed, when it became apparent late on election night that Donald would become the 45th President of the United States, markets tanked world-wide and gold and silver soared. Within twenty four hours the markets reversed course, apparently convincing themselves that a Donald Trump Presidency would be good for the markets as his proposed infrastructure spending and tax cuts would boost the economy.

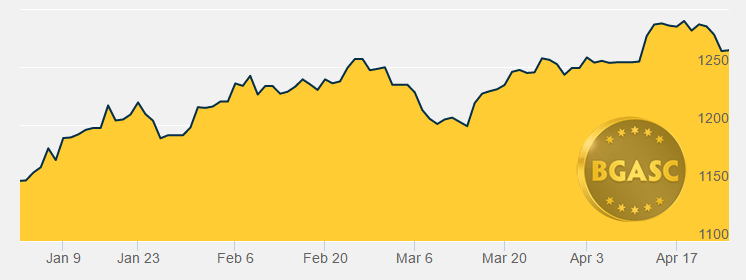

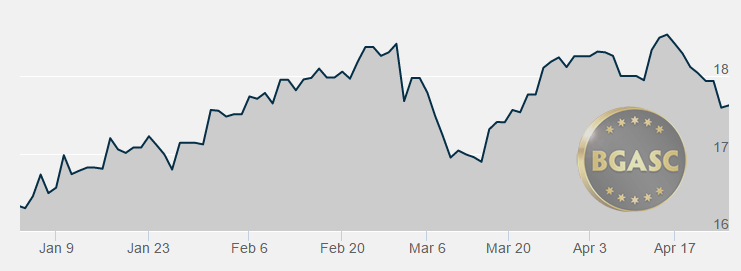

During the period from the election to Trump’s inauguration, stock markets soared and gold and silver gave up much of their gains from earlier in 2016. After Trump took office, stock markets continued their climb higher and gold and silver joined the party, both turning in double digit returns through mid-April.

In December 2016, during Trump’s transition, he met with Bernard Arnault, the CEO of luxury goods conglomerate LVMH, maker of Louis Vuitton and Fendi leather goods and Hennessy cognacs. Mr. Arnault sensed an opportunity in the expectation of Mr. Trump delivering on his campaign promise of lower personal and corporate taxes, that consumption of luxury goods in the United States would increase. Messrs. Arnault and Trump also reportedly discussed manufacturing opportunities for LVMH in the United States.

The Trump Cognac Effect (Greed)

LVMH’s reported stellar first quarter 2017 financial results that showed a 16% increase in revenues, driven by a near 30% increase in sales of Hennessy cognacs in the United States, confirming the anticipated Trump Cognac Effect . Higher stock prices and soaring consumer confidence have helped boost sales of luxury goods in the United States. Indeed, LVMH warned that if the pace of sales of Hennessy cognac in the United States continued at their torrid first quarter pace, there would be shortages of the amber liquid later this year, a shortage that could not be met by increased US production, as cognac can only be produced in the Cognac region of France.

Fear Dissipates, For Now

While the prices of gold and silver have risen since Trump’s inauguration, driven by strong Chinese and Indian demand and growing US institutional demand for precious metals ETFs, bullion sales in the form of coins and bars have stagnated. Retail sales of gold and silver bullion from the United States Mint and other sovereign mints constitute a small percentage of overall gold and silver demand, but are a good barometer of the sentiment of a segment of the population that is concerned about the economy, inflation, geo-political issues and the financial status of the United States. When this segment loads up on gold and silver bullion, it generally reflect a higher level of concern about the state of the economy and geo-political issues. Gold and silver bullion sales abate when these concerns lessen. Sales of gold and silver bullion at the United States Mint have declined steadily since January, perhaps indicating a pause in cause for concern.

Reversal of Fortune?

The current luxury consumption boom may not last. First quarter GDP estimates have been slashed and incoming economic data doesn’t support rising consumer confidence that is predicated on future expectations of lower taxes and global economic and geo-political stability. Inflation concerns may return to the fore later this year as the impact of a lower dollar and Trump’s 20%+ tariff on imported Canadian lumber and other tariffs impact pricing on imported and finished goods like houses and other consumer products. Consumer spending accounts for 70% of U.S. GDP. A good portion of that spending is on imported consumer goods. Any appreciable increase in the prices of those goods could curtail consumption. If the economy fails to accelerate later in the year, the stock market may also stagnate or fall.

While markets recently conducted a relief rally after the French elections failed to provide a compelling case that anti-Euro candidate Marine Le Pen might ultimately prevail her quest for the French Presidency, the geo-political scene is not without risk. North Korea and Iranian nuclear ambitions may be challenged by a Trump administration leading to turmoil and uncertainty. Issues surrounding Syria were not settled by the U.S. missile strike earlier this month. There are also potential trade wars looming between the United States and its trading partners like China, Japan, South Korea, Taiwan, Switzerland and Germany, whom the administration has put on its currency manipulator watch list. The North American Free Trade Agreement (NAFTA) between the United States Canada and Mexico is also subject to renegotiation or elimination. The imposition by the United States of a 20%+ tariff is probably the first salvo in the Trump Administration’s war on NAFTA.

Fear and Greed

Markets are driven by fear and greed. For now, greed, as represented by soaring stock and luxury good prices, appear to have the upper hand. Fear, however, is always lurking in the background. Market sentiment can change quickly. We will be keeping an eye on the sale of luxury goods and gold and silver bullion for any change in sentiment.

This article by BGASC is not, and should not be regarded as, investment advice or as a recommendation regarding any particular course of action.